- Small Business Statistics

Research Summary. In 2026, understanding the landscape of small business lending is crucial for entrepreneurs seeking funding for property, renovations, or investment. The following statistics highlight the current trends in small business lending across the U.S.:

-

Large, nonlocal banks account for 89.5% of smaller loans (less than $100,000) issued to small businesses.

-

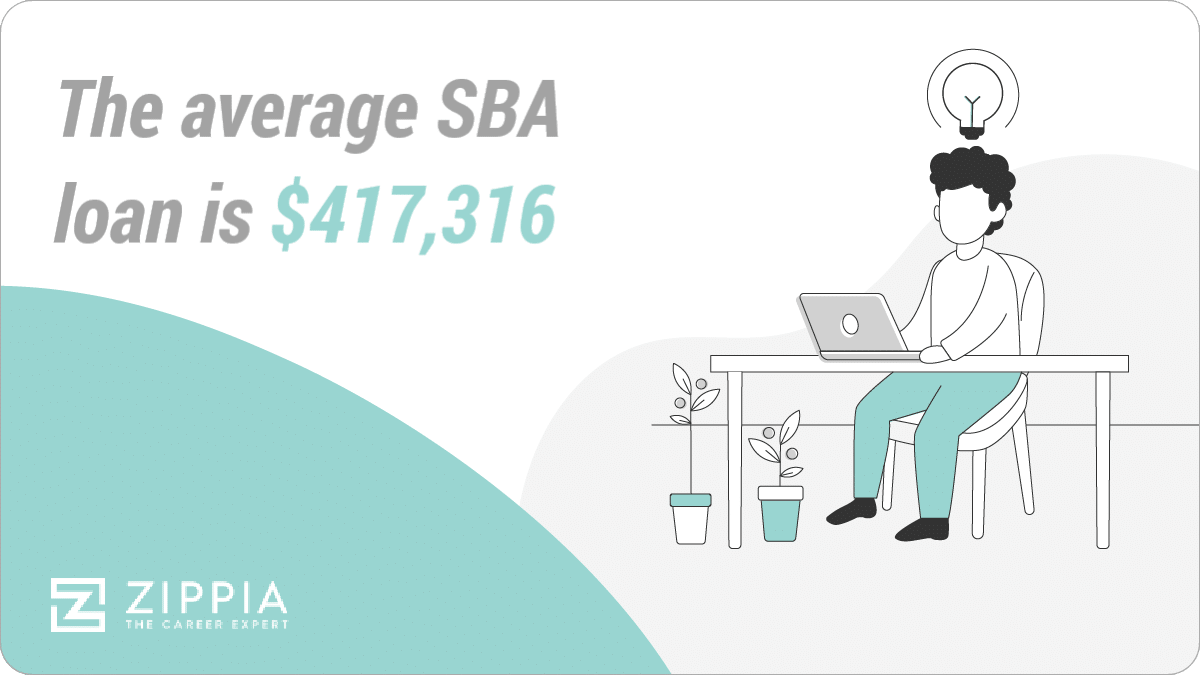

The average SBA loan is $417,316, with a maximum loan amount reaching $5 million.

-

SBA loans boast a 49% approval rate at small banks.

-

At large banks, the approval rate for SBA loans stands at 25%.

-

33% of small business owners face challenges or fail due to a lack of capital.

-

In 2020, the SBA facilitated over 14 million loans totaling $764 billion to small businesses.

For further analysis, we have categorized the data into the following sections:

Loan | Application | Demographics | Industry

Small Business Financial Statistics

Running a small business in the U.S. can be costly, and many entrepreneurs rely on loans to kickstart their ventures. Here are some key financial insights:

-

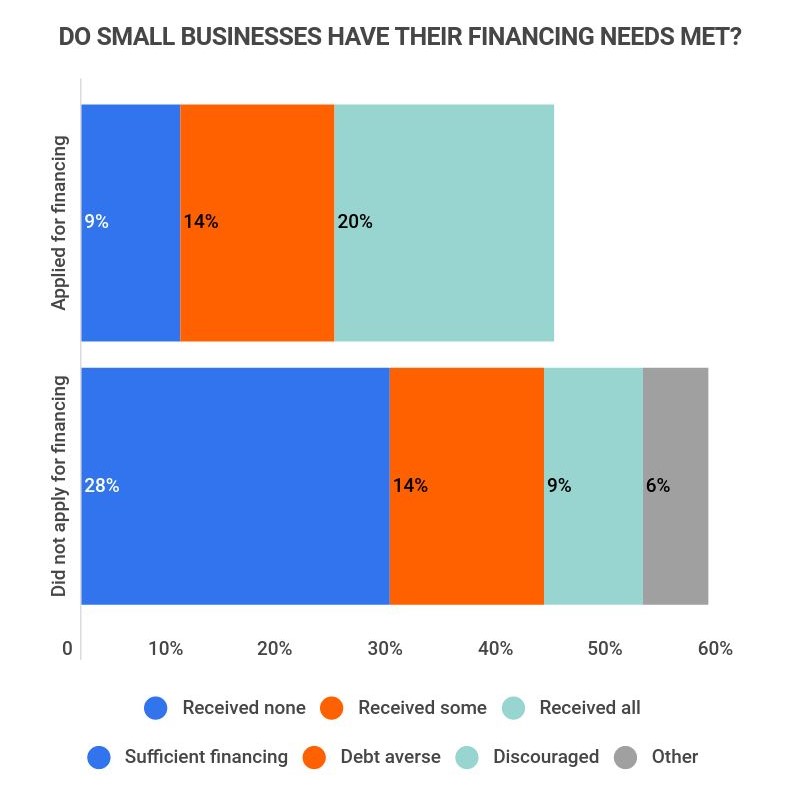

Only 48% of small businesses in the U.S. have their financing needs met.

This includes 20% of small businesses that secured loans and 28% that lacked sufficient capital without loans. Conversely, 52% of small businesses either receive no financing, receive only partial financing, or are too indebted to apply for loans.

-

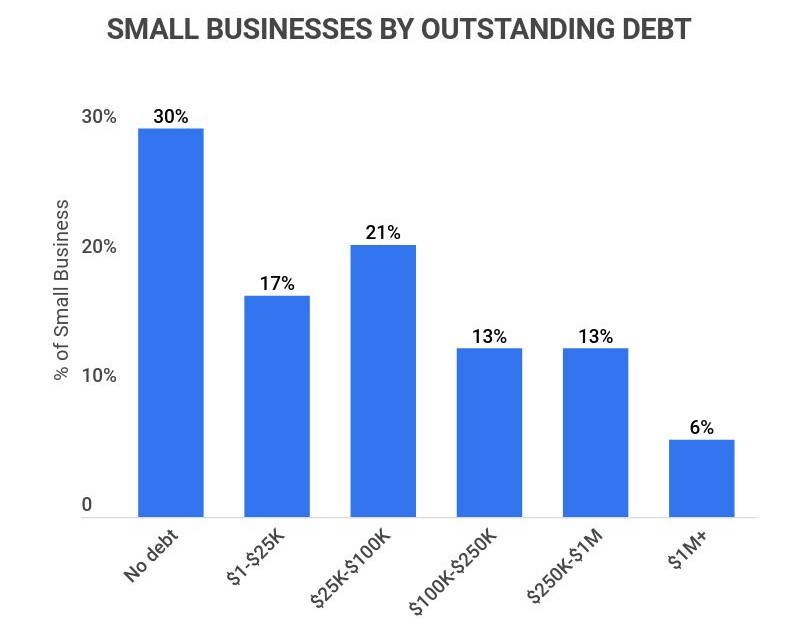

At least 70% of small businesses in the U.S. carry outstanding debt.

While nearly three-quarters of businesses are in debt, 38% owe less than $100,000, with 17% owing $1 to $25,000 and 21% owing between $25,000 and $100,000.

-

The average Small Business Administration (SBA) loan is $417,316.

The maximum loan amount for a standard loan is up to $5 million, while smaller SBA loan types cap between $350,000 and $500,000. Furthermore, most loans exceeding $25,000 require the lender to secure some form of collateral.

-

Only 38% of small businesses took out loans to expand in 2020.

The pandemic significantly impacted small businesses, with the percentage of those obtaining loans for expansion dropping from 58% in 2019 to 38% in 2020. Many businesses resorted to loans merely to survive.

-

The average interest rate for a small business loan is between 2.54% and 7.01%.

This variation is largely influenced by the lending institution and the loan program. For instance, SBA loans typically have interest rates ranging from 5.50% to 8%.

-

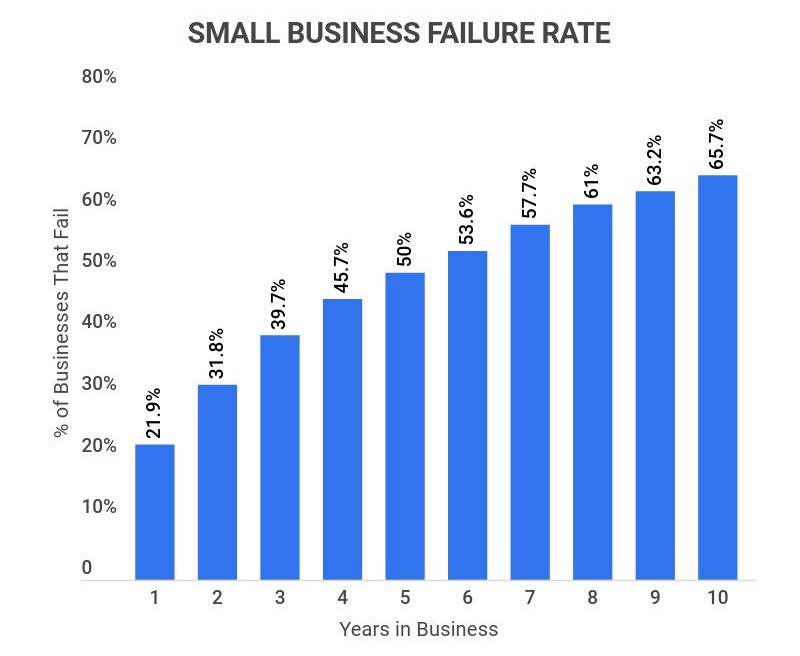

Only 33% of small businesses will survive for ten years.

While 79.8% manage to survive their first year, survival rates decline over time, with only 69.2% making it to two years and 50.2% reaching five years.

Small Business Loan Statistics

Many businesses rely on loans for expansion, and in recent years, the need for loans has remained critical. Here are current insights into small business loans:

-

The average small business loan is now $633,000.

This figure encompasses both smaller regional and large banks, but highlights the significant range of loan amounts available. A small business can typically secure anywhere from $13,000 to $1.2 million from banks.

-

In 2020, the SBA distributed over 14 million loans worth $764 billion to small businesses.

Notably, $736 billion of this amount was allocated to COVID-19 relief loans, indicating that 96% of the loans distributed by the SBA that year were focused on pandemic recovery.

-

The average small business loan from alternative lenders ranges from $50,000 to $80,000.

These alternative lenders are often private companies operating online, including well-known names like Fundbox, BlueVine, and OnDeck.

-

The average loan amount from large national banks is $593,000.

In contrast, small regional banks typically lend an average of $146,000. Interestingly, foreign banks extend an average of $8.5 million to small businesses.

Small Business Loan Application Statistics

Applying for loans can be a daunting process, but it’s a necessary step for many small businesses. Here are the latest statistics on small business loan applications:

-

43% of small businesses applied for a loan in 2020.

Many of these businesses sought COVID-19 relief, underscoring the struggles faced by nearly half of American small businesses during that period.

-

Loan approval rates for small businesses applying to large banks are only 13.8%.

In contrast, small banks offer approval rates up to 19%, while non-bank loans have an approval rate of 24.7%. Overall, these rates are considerably lower than those for SBA loans.

-

32% of small businesses now apply to non-bank lenders.

This marks an increase from 24% in 2017 and 19% in 2016, reflecting a growing trend of businesses seeking alternative funding sources.

-

20% of small business loans are denied due to credit issues.

If a small business has poor or no credit, this can significantly affect their chances of securing a loan. It’s important to monitor both business and personal credit scores.

Small Business Loan Demographics

Disparities exist in loan access based on geographic location, race, and gender. Here are some notable demographics regarding small business loans:

-

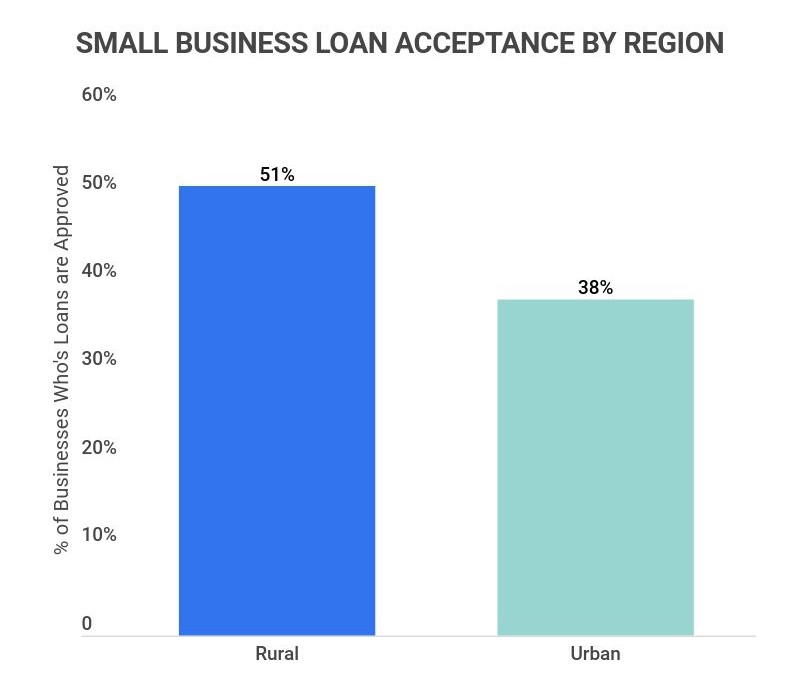

Rural small businesses are more likely to receive loans, with 51% acquiring all requested financing.

In comparison, only 38% of urban small businesses receive the full financing they request, despite urban areas housing 83% of small businesses.

-

Rural small businesses are more reliant on small banks, with 62% of loan applications directed to them.

Conversely, 53% of urban small businesses apply to larger banks, with only 43% seeking loans from smaller banks. This is reflective of the higher concentration of small banks in rural areas (55%) compared to urban settings (25%).

-

Black-owned businesses receive less than 2% of small business loans.

This is concerning, given that Black Americans represent 13% of the population. Studies indicate that Black-owned firms are twice as likely to face loan rejections, with only 47% of their financing applications approved.

-

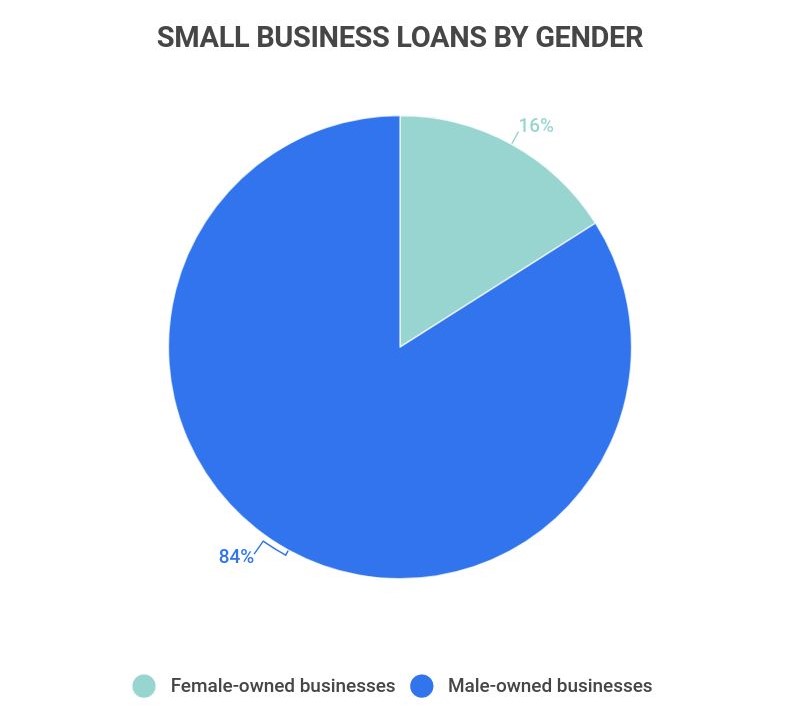

Women-owned small businesses receive only 16% of small business loans.

This statistic is particularly striking considering that women own approximately 30% of small companies. Research has shown that women are often subjected to stricter loan terms compared to their male counterparts.

Small Business Loan Statistics by Industry

The industry in which a small business operates can significantly influence loan approval rates. Here are some insights into small business loans by industry:

-

The construction and renovation industry receives the highest proportion of small business loans, roughly 15%.

Transportation and trucking small businesses also receive around 15% of the loans, as they typically require financing for equipment, repairs, and maintenance.

-

Full-service restaurants received the highest volume of SBA small business loans, totaling 28,680 in 2019.

Limited-service restaurant businesses ranked second, with 19,141 loans distributed. The combined total for these loans exceeded $17.1 billion. The dental industry followed with 10,699 loans totaling $6 billion.

-

At least 11 potentially legal industries are ineligible for SBA small business loans.

These include gambling, government-owned entities, loan packaging firms, multi-sales distribution, nonprofits, MLMs, real estate investment firms, religious organizations, and speculation-based industries.

Small Business Lending FAQ

-

What percent of small business loans are approved?

General small business loans have a 57% approval rate, while SBA loans offer a higher or lower approval rate depending on the bank’s size. Approval rates are also influenced by the applicant’s location, bank type, and demographic factors such as race or gender.

For instance, rural small businesses enjoy a 51% approval rate compared to just 38% for urban businesses.

This disparity arises because urban businesses often rely on large banks, which have approval ratings as low as 13.8%, whereas small banks have a significantly higher approval rate.

Moreover, minorities, including Black Americans, face challenges, with only 47% of loan applications from Black individuals being approved.

-

How are most small businesses financed?

Most small businesses are financed through the owner’s personal investments. This encompasses savings and personal assets. Even during the peak of loan applications in 2020, only 43% of small businesses sought a loan.

When financing is needed, the most common sources include: the SBA, large national banks, small regional banks, and alternative lenders, which can offer loans ranging from a few thousand to over a million dollars.

-

Is small business lending profitable?

Small business lending can be profitable, though it also carries risks. Higher interest rates can make loans lucrative for lenders, and larger loans, like a $500,000 loan, may take as long to repay as a mortgage, allowing substantial interest to accrue.

Conversely, smaller loans (under $25,000) may not be profitable for lenders, and those viewing a business as too risky may decline to finance it, as failure would result in significant losses.

-

How much debt does the average small business have?

In the U.S., the average small business owner carries about $195,000 in debt. It’s crucial to note that a small business’s debt should ideally not exceed 30% of its overall capital.

-

How do small businesses qualify for loans?

To qualify for loans, small businesses should follow four basic steps:

-

Build Credit. Establishing a strong credit score is essential for qualifying for any loan, including those for small businesses. This can involve improving personal credit or developing solid business credit.

-

Research Qualifications & Requirements. Understanding the qualifications for a loan is vital. Research different loan types, especially the key differences between federal and bank loans.

-

Gather Documents. Essential financial and legal documents must be prepared to qualify for a small business loan. This might include personal and business tax returns and commercial licenses.

-

Present a Business Plan. A well-crafted business plan can instill confidence in potential lenders. This plan should encompass a company description, product/service details, market analysis, operational plans, and financial forecasts.

-

-

Can you get a business loan with no revenue?

Yes, obtaining a small business loan without revenue is possible. Though it can be challenging, many startups rely on loans to launch operations.

To enhance your chances of securing a loan without revenue, consider the following:

-

Credit. A high credit score can significantly improve your chances of obtaining a loan.

-

Financial Projections. Providing realistic financial forecasts can instill confidence in lenders regarding your business’s potential profitability.

-

Business Plan. A comprehensive business plan helps investors understand your offering and its market viability.

Additionally, consider alternative funding methods such as business credit cards or crowdfunding initiatives.

-

-

What credit score do I need for an SBA loan?

Aiming for a credit score of at least 690 is advisable when applying for an SBA loan. Scores between 690-720 generally yield good odds, while scores above 720 significantly improve your chances.

While it’s feasible to secure an SBA loan with a credit score below 690, it can be more challenging. Lenders may be deterred by concerns regarding repayment history and the potential for business failure.

Conclusion

In 2026, securing financing is more critical than ever for small businesses, as 33% of owners cite inadequate capital as a primary reason for struggles or failures, and only 48% report meeting their financing needs. Notably, 43% of small businesses applied for loans in 2020, highlighting the ongoing necessity for funding.

Despite the average small business loan ranging between $400,000 and $650,000, depending on the lender, approval rates hover around 57%, often leading to denials due to creditworthiness and capital constraints.

Fortunately, small businesses have several financing avenues available, including the SBA, large national banks, small regional banks, and alternative lenders, allowing them to navigate their funding needs more effectively.

Sources:

-

Federal Reserve Banks. “Small Business Credit Survey.” Accessed on November 22nd, 2021.

-

SBA. “Types of 7(a) loans.” Accessed on November 22nd, 2021.

-

Nerdwallet. “Average Business Loan Rate: What to Know About Interest Costs.” Accessed on November 22nd, 2021.

-

Entrepreneur. “The True Failure Rate of Small Businesses.” Accessed on November 22nd, 2021.

-

ValuePenguin. “Average Small Business Loan Amount: Across Banks and Alternative Lenders.” Accessed on November 23rd, 2021.

-

SBA. “SBA Achieves Historic Small Business Lending for Fiscal Year 2020 with More Than $17 Billion in SBA Seattle District.” Accessed on November 23rd, 2021.

-

Small Business Trends. “Small Business Loan Approval Rates Up at Big Banks.” Accessed on November 23rd, 2021.

-

FRB. “Access to Financial Services Matters to Small Businesses.” Accessed on November 23rd, 2021.

-

FORA Financial. “4 Steps to Take If You Aren’t Approved for an SBA Loan.” Accessed on November 23rd, 2021.

-

Fundera. “Rural Small Businesses Earn Better Profits and More Financing vs. City Ones.” Accessed on November 23rd, 2021.

-

The Guardian. “Black-owned firms are twice as likely to be rejected for loans. Is this discrimination?” Accessed on November 23rd, 2021.

-

Ondeck. “How the Gender Gap Affects Small Business Loan Approvals.” Accessed on November 23rd, 2021.

-

FORA Financial. “The Industries Most Likely to Ask for a Business Loan and Why.” Accessed on November 23rd, 2021.

-

WestTown Bank & Trust. “The Top 40 Industries for SBA Financing in 2020.” Accessed on November 23rd, 2021.

-

SBA. “Does Your Industry Qualify for an SBA 7(a) Loan? Will You Benefit?” Accessed on November 23rd, 2021.

- Small Business Statistics

Author

Jack Flynn is a writer for Zippia. In his professional career he’s written over 100 research papers, articles and blog posts. Some of his most popular published works include his writing about economic terms and research into job classifications. Jack received his BS from Hampshire College.