Find a Job You Really Want In

How Long Will Economic Challenges Delay Boomers’ Retirement?

For many Americans, work is merely a means to an end, with retirement representing the ultimate goal. However, for baby boomers approaching retirement, this dream may feel increasingly distant.

As financial markets experience volatility, baby boomers are faced with a critical decision: Should they withdraw their retirement savings during a downturn, or should they continue working in hopes of a market recovery? Can they maintain their positions in the workforce long enough to secure a comfortable retirement?

While some may dismiss concerns about the market’s fluctuations, many boomers working traditional hours find that time is not on their side. Indeed, time is a luxury that many do not possess; approximately 48% of retirements occur unexpectedly due to health issues, caregiving responsibilities, or layoffs.

We analyzed the current economic landscape to understand how these financial challenges may affect baby boomers’ retirement timelines and their overall financial well-being.

Summary

- Boomers saving for retirement may need to postpone their retirement by up to 4 years to recover their savings.

- If targeting a retirement age of 65, this delay would mean working until age 69.

- Those who started saving later may fall even further behind.

- Boomers who face job loss or pay cuts will find it more difficult to contribute to retirement savings and may be more severely impacted.

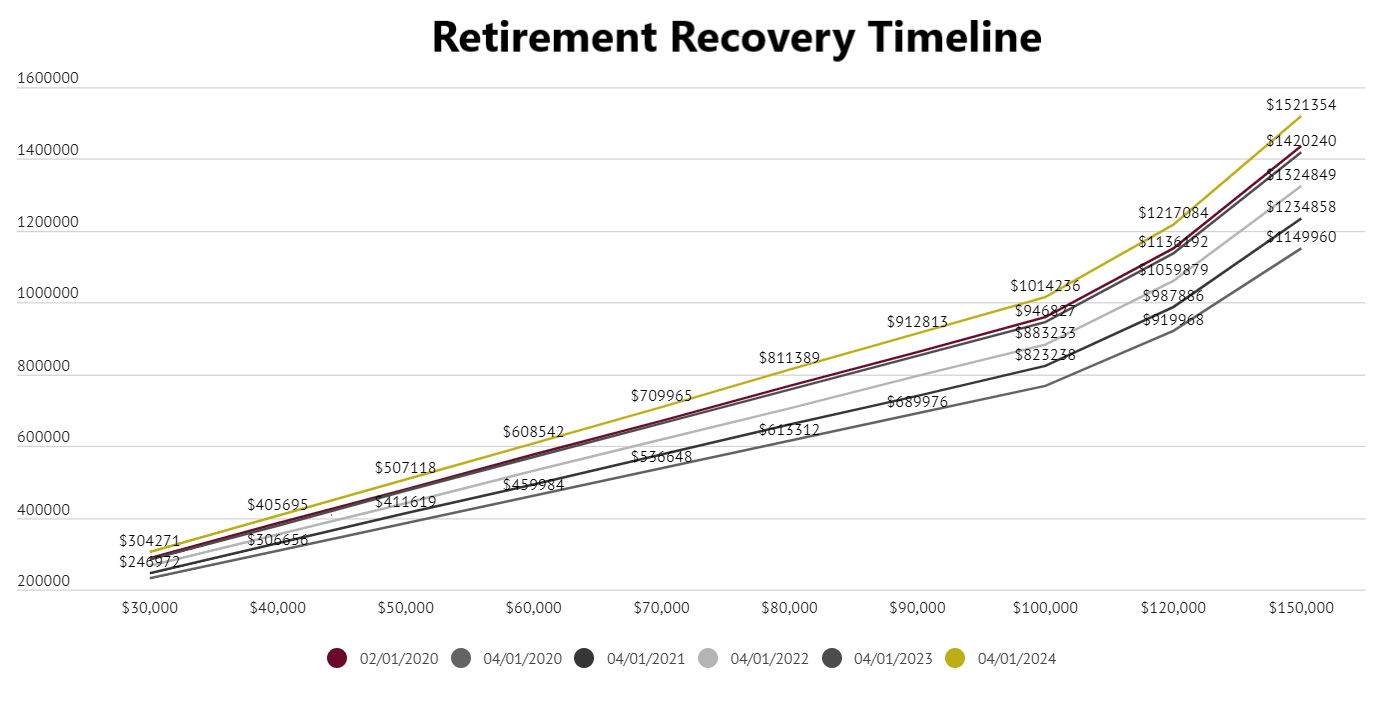

It takes approximately four years for retirement savings across all income levels to surpass the amount held in February 2020. A three-year period brings savers close to that number but falls short. Increasing contributions or downsizing lifestyle expenditures can expedite this timeline. Nonetheless, retirees at every income level will face difficult choices if they wish to retire sooner rather than later.

How We Assessed the Impact on Boomers’ Retirement

To evaluate how market downturns are affecting boomers’ retirement plans, we first established the savings needed for retirement. Experts recommend that boomers save enough to withdraw approximately 70% of their pre-retirement income annually. For those with unpaid mortgages, dependents, or significant plans, this figure may need to be higher. We calculated the necessary savings based on various income levels ranging from $30,000 to $150,000.

We considered both an “average retirement” duration and a “lifetime expectancy” scenario. The average retirement lasts around 18 years, while a lifetime expectancy presumes retirement ends at or before the average lifespan of 78—five years shorter than the average retirement period. Our model illustrates the shorter life expectancy retirement, but both scenarios yield similar recovery rates for savings.

Assuming a 20% drop in savings, we projected how quickly retirement accounts might grow with participants continuing to work and contribute 10% of their pre-tax earnings, alongside a conservative 6% annual growth rate.

This assessment assumes boomers are generally on track for retirement. Those who are behind and investing aggressively to compensate for late starts will likely experience even greater setbacks. Additionally, those who lose jobs or face financial hardships and cannot contribute to retirement funds will be hit harder than those who maintain their positions and continue investing.

All data is based on a retirement target age of 65. We hope that older boomers have already built robust retirement accounts and are enjoying their dream retirements. If not, the path to retirement may be lengthier than anticipated.

Final Thoughts on Boomers’ Delayed Retirements

Four years may not seem significant for younger workers, but for boomers nearing retirement, it can feel like an eternity.

In reality, four years might be too long. Many older workers may lack the health or energy to remain in the workforce until age 79. Even those in good health might encounter challenges finding new employment due to age discrimination or shifting job market dynamics. An older worker’s ability to secure a new position after 65 can be significantly hindered.

What does this imply? It suggests that an increasing number of seniors may retire with diminished resources. Some may hope to recover their investments post-retirement, while others may opt to reduce expenses and stretch their retirement savings as far as possible.

Author

Kathy is the head of content at Zippia with a knack for engaging audiences. Prior to joining Zippia, Kathy worked at Gateway Blend growing audiences across diverse brands. She graduated from Troy University with a degree in Social Science Education.